Predictive Analytics improves M&A Activity

There have always been two major ways to expand your business: Grow it, or Buy it. This brings up some interesting questions about which is more beneficial. The correct answer is usually based on cost of customer acquisition and customer lifetime value. Right now, with the cost of client acquisition being so high, companies are turning to buying distressed businesses. One, it eliminates competition, and two, the customers can be acquired “on sale”. While mergers and acquisitions are common across all industries, there seems to be a significant propensity for growth by buying in the banking industry.

The unique problem that is causing an increase in the ” buy them” thought process is that in banking their revenue generating power has dwindled with the decline of interest rates. Not only that but as clients leave for competitors by natural attrition, there is a dire need for new customers. Buying seems to solve both of these.

While it may solve the issue of new customers at a reduced cost, how to transfer the old customer base to the new bank has always been a major problem. First, you have a bevy of new customers who have not gone through your buying process. You have no idea who they are and why they are in the product they are in. Secondly, you can fix problem number one by keeping the staff from the bought bank, but they’re not sure if the customers are in the correct products anymore either because they don’t know what products they have to sell.

There are two ways used to combat this new problem of keeping old customers. You can train the bought bank staff to re-sell or use the buying bank staff to cross-sell. In the past, the new bank circumnavigated this problem by not calling the individual customer. They simply sent a mailing to each new customer hoping they opened it, called, and stayed because they found the new bank was better. With the overuse of mailings and sales calls, people have become immune to this tactic. It isn’t effective anymore. People want to be called in this instance. Training the bought staff takes them away from the process of selling the old customer base on reasons to stay with the new bank, and using the buying bank staff takes them from their customer service duties to the buying banks original customers putting those clients in jeopardy of leaving. It is actually quite a mess.

Solving which sales team brings up another problem. Most sales teams aren’t equipped to resell and retain customers. This stems from the fact that the average salesperson only recommends 8 different products regardless of how many they have to sell. It turns out the human brain is to blame. Sales people have a capability to discern and keep track of only limited number of products. This means that when they are calling on your new, bought customer base in an effort to put them in the right product, they physically can’t know all 70 or 80 bank products well enough to put them in the best product for them and for the bank.

There’s more.

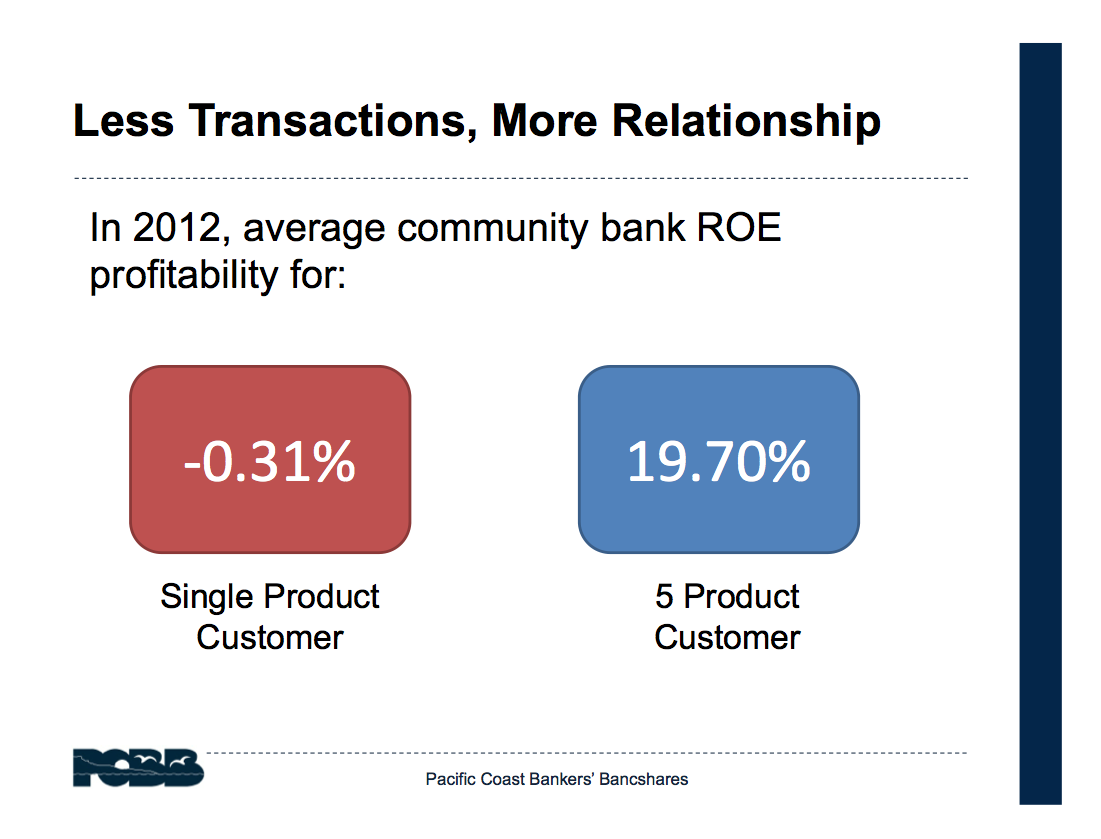

In a presentation given during the Community Banking Conference, Steve Brown, President and CEO of Pacific Coast Bankers’ Bancshares gave a revealing stat for community banks. The ROE (return on equity) from a single product customer last year was -.31%. But, if you have a 5 product customer, the ROE climbs to +19.7%. A 20% swing. This means that not only do you need to save these new, bought customers, but you need to move them to at least 2 products be profitable.

So now we have a huge customer base, with loads of data, who you have to call them to keep them from leaving, and you have to sell them more.

I told you it was a mess.

There is a way. Because of technology and the fact that banks collect mountains of data on their customers, there is a way for the new bank to reach out to the old bank customers and instead of guessing what they want (which just makes customers mad), know what they want. You can know what products would save them money, where they were in the banking sales relationship, and what is needed to be conveyed to the customer to get them to stay. Not as a sales process, but as a “we want to take care of you and give you the products you want” process.

It’s called Predictive Analytics. It works because it identifies, using math, which customers are at highest risk so a salesperson can contact them. It means salespeople aren’t frozen by thousands of names to call, they just have a ranked and prioritized list. It can be updated weekly, monthly, or quarterly as needed. Predictive Analytics used to be only for the big boys because of the price and availability, but because of a slew of new players to the market in the last few months, the cost has plummeted to the point that community banks and credit unions now have access to trends, algorithms, and sales patterns.

There are a number of solutions (including ours) that aid in the process of up-selling, cross-selling, and retention. The one you should pick should at least do the following:

- Tell you who to call first– Your program should prioritize which customers have the highest chance of leaving. You should call those customers first as keeping those not afraid to go will stem some of the tide leaving behind them. Note: It should do more than just describe them like Business Intelligence systems are known for, it needs to tell you by name who to call for it to be valuable.

- Tell you what to sell to them– It may be as simple as selling them an auto loan. But which one? At what rate? Remember, the average salesperson can only remember 8 products. You need something that is going to be able to predict which product works best for each customer.

- Tell you which customers should be moved to different products– You have new products, different products, and more importantly, should want your customers in the correct products. A predictive model should be able to predict which product each customer should be in based on your current customer data.

- Be a service. There are at least 10 softwares out there that promise these results. They work, but you have to do them. You have to learn them, install them, and assign someone to be in charge of running them. You’re a bank. You are great at loans and customer service. This is math, complex math, designed and done by people who spend their whole lives creating algorithms for just this kind of use. You can also build the skill in-house, but that gets expensive and the talent is rare. We recommend a service. The person who runs it can’t quit, leave for a competitor, or be out of date. They will help you with implementation and political red tape as well. The fact that a third-party is making recommendations also leads credibility and backs up the vision you have been trumpeting for years as a manager. We recommend you choose a service that has done work for banks, and has security to protect your sensitive data. Whether to buy or build predictive analytics.

These are just the minimums. These are the characteristics you will have to have for your sales team to be able to keep the customers you are buying and keep happy the customers you already have. You just have to pick one.

Otherwise, you run the risk of losing customers and salespeople from both banks. and that benefits no one.

Learn more about the benefits of Predictive Analytics with our eBook:

[contact-form-7 id=”4042″ title=”Predictive Analytics eBook – Predictive Analytics improves M&A Activity”]